Options for associate compensation

When you finally decide it’s time to bring on an associate, many questions come to mind. Some immediate ones include: When is the best time to bring on an associate? How are new patients going to be assigned? For what procedures will the associate be responsible? And, of course, how will the associate be compensated?

The main theme of this article is options for determining associate compensation, but there are many related questions that arise when determining the associate compensation formula and the associate’s employment agreement with the practice. Examples of these questions include:

- What qualities should I look for in an associate?

- Is this “just a job” for the associate, or is this his or her future?

- How will the associate’s hours be broken down on a daily and weekly basis?

- For tax purposes, is the associate an employee or an independent contractor?

- Can my facility support an associate?

- Will the team and patients accept the associate?

- Will the associate be compensated differently depending on the procedure (e.g., endodontic procedures, clear aligners, routine extractions, etc.)?

You might also want to read:

Your associate doctor: Benefit or bust?

New associate's potential ownership; building production as a part-time associate

Each market is different, but based on feedback from my colleagues in the Academy of Dental CPAs, an average compensation offer to a general dental associate typically uses one of the following formulas:

- Percentage of collections

- Percentage of production

- Annual fixed compensation

- A hybrid formula

Let’s look at each of these individually and see which might make sense for your practice.

Percentage of collections

Most associates are offered 35% of collections. Alternatively, some associates are offered 35% of collections less 35% of their lab fees. Still others are offered a straight 33% of collections.

For practices using CAD/CAM technology, lab fees will be different from practices with a more traditional lab arrangement. It probably makes sense for practices using CAD/CAM to include what the cost per unit will be in the employment contract. If this applies to you, consider anywhere between $50 to $80 per unit to take into account the cost of the porcelain block, equipment, and related overhead.

When I run the numbers using a compensation formula of 35% of collections less 35% of lab fees, it nets 33% of collections. You may want to consider running the numbers with your practice and comparing your results to mine.

Percentage of production

Some associates are paid a percentage of production. In this case, the percentage is normally less than the percentage of collections. This is because the employer doesn’t consider bad debts or uncollectible accounts.

Production is defined as “net production,” which takes into account insurance write-offs, adjustments related to explanations of benefits, senior citizen discounts, and professional courtesies. I usually see the percentage of production number in the neighborhood of 25%.

Annual fixed compensation

To remain competitive, especially against corporate dentistry, I feel you should offer your associate a starting base salary in the range of $125,000 to $150,000 annually. This is considered base compensation.

If you choose this path, I would highly recommend you consider including incentive compensation within your employment offer as well. Incentive compensation is paid in addition to base compensation.

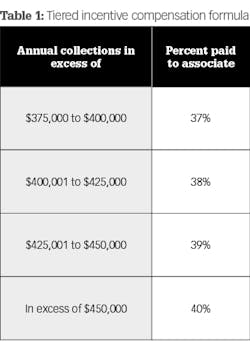

Let’s look at an example. Say the associate’s base compensation is $125,000, and the practice has chosen an incentive compensation ratio of 3:1. This means that if the associate’s annual collections exceed three times his or her base salary, which would be $125,000 x 3 = $375,000, the tiered incentive compensation formula in Table 1 would apply.

Let’s say that the associate under this incentive compensation formula produced and collected $460,000 for the year. The associate’s compensation would be calculated as shown in Table 2. As you can readily see, if we add the base compensation to the incentive compensation, the associate’s total annual compensation is $157,500. This translates to an effective compensation rate of 34.2% ($157,500 in compensation divided by $460,000 in collections).

Hybrid compensation formula

A third associate compensation formula combines elements of those previously discussed, and also accounts for specialty procedures not currently offered in the practice. This might include services such as endodontics or clear aligners. A possible hybrid compensation formula is outlined in Table 3.

As shown in Table 3, the associate’s annual compensation would be $169,000. If the total annual collections of the associate were, say, $467,000, this would calculate to an effective compensation rate of 36.2% ($169,000 in total compensation divided by $467,000 in total collections).

Fringe benefits

In addition to the compensation options we’ve discussed, you might also want to consider any of the following fringe benefits:

- Malpractice insurance

- Meals

- Entertainment

- Professional dues

- Continuing professional education

- Travel

- Cell phone

- Automobile

You might want to add some if not all of these benefits as you develop a stronger relationship with your associate. For example, if you expect your associate to help you expand your practice by acquiring new patients, you may want to give a marketing budget to your associate. This is done by creating a monthly allowance for your associate to develop a patient base and referral sources in the practice.

Other important considerations

Insurance credentialing: If your practice is participating with various insurance companies, you will need to get your associate credentialed. This must be done prior to the associate’s performing of professional services and the submitting of services as insurance claims. During the credentialing process, most employers offer a minimum per diem that could range between $500 and $600 a day.

Freeze the practice value—now! Consider “freezing” the value of your practice now, prior to the associate joining you. If you do not, the associate may think, “Why should I produce and build this practice, only to have to pay for the increase in value I generate from my own efforts?” In effect, if you do not freeze the value of the practice, you might be creating a disincentive within the compensation agreement.

Covenant not to compete: Within the compensation agreement, consider a covenant not to compete (CNTC). This will protect you and the practice in the event you and your associate part ways. Through the years, I have found that it may take about three associate hires to finally land the one who truly believes in your practice philosophy.

Please consult your dental CPA and dental-specific attorney for the parameters surrounding a CNTC within the your specific market.

Independent contractor or employee? In most cases, and under current tax law, your associate is considered an employee and not an independent contractor. This is because you provide the tools (facility, workforce in place, schedule, etc.) for the associate to provide professional services to your practice. Unfortunately, this means added costs to you as the employer with respect to payroll taxes, workers’ compensation insurance, and related fringe benefits.

Please check with your dental CPA as to the classification of your associate. Take note that this issue is one of the “dirty dozen” in the IRS audit process. This is due to abuse of employee classification within the dental profession.

As you can see, the issue of associate compensation in your practice is a complex one. There are many variables that must be considered in arriving at a fair arrangement.

It may make sense for you to engage a dental CPA along with a dental-specific attorney to help assist you in the crafting of an agreement. After all, you want to make this arrangement a win-win for you and your associate. Good luck with the process!

Editor's note: Originally posted in 2020 and updated regularly

About the Author

Allen M. Schiff, CPA, CFE

Allen M. Schiff, CPA, CFE, is a founding member of the Academy of Dental CPAs. This group of very knowledgeable CPA firms specializes in practice management services for the dental industry. He serves on the ADCPA executive committee and is the current president of the ADCPA. Reach him at (410) 321-7707 or [email protected].

Updated February 20, 2019