Unpacking dental practice transitions before booking your destination

Key Highlights

- Price and value aren’t the same: Price reflects market supply and demand, while value is shaped by profitability, culture, location, growth potential, and other practice-specific factors.

- Most valuations come down to cash flow: Normalized operating cash flow—adjusted for nonoperating, nonrecurring, and discretionary expenses—is the core driver of practice value and loan affordability.

- DSO deals require deeper modeling: Beyond the headline sales price, DSO/PE transactions involve EBITDA-based valuations, equity structure, earnouts, and long-term financial tradeoffs that should be stress-tested with scenario analysis.

For many dentists, buying or selling a practice is the most meaningful business transaction of our professional lives. Therefore, it is incumbent on us to strategically find the right fit as a buyer and the right exit as a seller. As a dental professional, I’ve purchased a practice, acquired another location during ownership, and sold my business. With each iteration, I learned actionable insights from advisors who helped sharpen my decision-making. I’ve enjoyed sharing my experiences with peers and later strengthened my knowledge by earning an MBA in finance, which galvanized me to more formally advise colleagues with practice transitions.

Price vs. value

Simply stated, price is what one pays to obtain a product or service. Price is concrete and derives from a market-clearing mechanism anchored to supply and demand. To the contrary, value is more equivocal as it measures the happiness delivered by a product or service. Despite the subjective quality of value, business finance presents frameworks to quantify it. Value is dynamic and a gestalt of the practice’s profitability, brand, culture, geographic location, trajectory, and more. As consultants, we work cohesively with clients to highlight the salient features relevant to value.

Valuations

The typical dental practice is worth more than its tangible assets. As members of ADS, a network of nationwide dental practice transition firms, our firm has access to information on how sales price relates to key metrics such as net collections. Given the nuances of each practice, advisors shouldn’t rely closely on industry data to compute sales price; nevertheless, market data provides parameters on whether appraisals are consonant with comparable transactions in that geographic region.

To appraise most dental practices, we apply an income approach for which the normalized operating cash flow (CF)—or some close proxy—is a critical data point for computing value. An income approach is preferable because CF underpins the buyer’s access to a practice loan and capacity to make loan payments. The term “normalized” represents the adjustments made to practice financials. Standard adjustments are nonoperating, nonrecurring, and discretionary. The objective is to remove expenses that are unrelated to operations, are not expected to recur, or reflect the seller’s personal business-related expenses (e.g., owner’s automobile lease payments). By removing superfluous expenses, we calculate a more accurate portrait of the business.

There are also comparability adjustments, which normalize expenses to industry benchmarks, but these adjustments are less compelling and should be used conservatively since expense and revenue line items are often entangled. Artificially reducing an expense without a corresponding decrease in revenue may be specious.

There are several factors beyond CF that impact value, including the payer mix, hygiene production, equipment condition, and local demographics and economics, among others.

Traditional (doctor-doctor) transaction

For concision, I’ll focus on two conventional income approaches for valuations. One is the discounted cash flow (DCF) method, which equals the expected free CFs discounted at the opportunity cost of capital. The opportunity cost of capital converts—discounts—future free CFs into their present value. To add and subtract free CFs, they must be in the same dollar units. DCF constitutes an explicit forecast period, which contains detailed projections for each year, and a continuing (terminal) value component.

While DCF is a robust technique, dental appraisals often enlist a capitalized income method that uses presale performance as a predictor of postsale performance. It upholds that previous operating CFs will be representative of the future and will change (e.g., grow) at a steady rate.

To capitalize CFs, the estimated economic benefit earned from the practice is divided by a capitalization rate, which embodies the potential risk and ROI. Consultants leverage their expertise to determine the capitalization rate by incorporating inputs such as the risk-free rate, equity risk premium, and anticipated growth rate.

The type of sale and the tax allocation of assets influence the final sales price, because these features have significant implications for liability and after-tax proceeds. Dental transactions are typically classified as an asset sale, ascribing 70%–90% of value to intangible assets. While allocations must comply with IRS codes, there is latitude with the precise classification in each deal to optimize the outcome for both parties. Additional factors may dictate the final sales price; for example, the number of prospective buyers or the seller’s urgency to retire. After all, fair market value is governed by a willing buyer and a willing seller.

DSO/private equity transaction

DSO transactions are ostensibly more complex because the seller’s proceeds are enveloped in much more than the sales price. For instance, proceeds from DSO sale encapsulate the postsale employment agreement, possible earnout clause, profit sharing or distributions, and equity stock performance. Additionally, DSO deals often use a different income approach, the EBITDA method, to compute practice value. Adjusted EBITDA is another permutation of CF (although not equal to actual cash) that facilitates comparison of practices since adjusted EBITDA is not affected by items unrelated to core operations, such as taxes.

A value proposition for DSOs is enabling providers to focus on their clinical competencies rather than on business management. DSOs can support doctors with administrative and marketing services, possibly unlocking time for doctors to be more productive in the clinic.

Not only do DSOs come in many flavors, but they also curate variable amounts of business nourishment. It’s important that doctors reflect on their motivations for joining a DSO. Is it to delegate HR, marketing, compliance, billing/collections, or insurance credentialing? Is it to extract value from the DSO’s business acumen, centralized services, negotiating power with suppliers, or access to capital for office investments? Is it to join a multispecialty practice model? Is it to be immersed in a collegial ecosystem with peers?

There are several cogent reasons to partner with a DSO. Furthermore, DSOs may harness the portfolio effect insofar as the variance (risk) of their asset is determined by the covariances of their partner practices rather than the variances of their individual practices. This phenomenon diversifies away the idiosyncratic (practice-specific) risk and thereby may attenuate the overall risk of the portfolio.

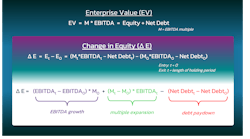

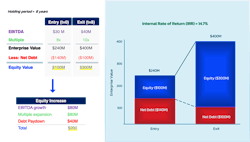

Although not applicable to all DSOs, private equity (PE) is frequently the engine behind consolidation, providing the capital to form and expand DSOs. In some circumstances, PE-backed DSOs may even have access to synergies with other portfolio companies. To best evaluate a DSO partnership, it’s constructive to first understand the mechanics of the PE industry. Broadly, PE has three equity growth drivers, which are illustrated in Figures 1 and 21:

EBITDA growth: This is an intuitive vehicle for equity growth. If a DSO increases its overall EBITDA, then this will enhance its equity value, ceteris paribus, reaffirming alignment with your goals to succeed. On the aggregate level, EBITDA can increase, notably, by top-line growth, bottom-line growth, and practice acquisitions.

Multiple expansion: The multiple may reflect the DSO’s profitability, but it may also hinge on the exuberance around the dental industry, competition with other bidders, interest rates, etc. For example, if a PE firm can borrow debt at low interest rates to finance an acquisition, then it may pay a higher multiple. As we’ve witnessed, this scenario may eventually pose challenges as markets often calibrate, elevating interest rates and encroaching on CFs to operate and reinvest in practices.

Debt paydown: This constitutes another opportunity for PE to create value. In theory, the debt paydown lever doesn’t require the asset value to increase for PE to capture a return. For the same enterprise value, PE can earn a return by decreasing net debt during its holding period. A common analogy is a rental home mortgage.

Other notable considerations are the types of DSO structures and equity stock issued. Three common structures are holding company (TopCo equity), joint venture (practice-level equity), and hybrid architectures. Moreover, DPOs introduce additional variety, often providing more autonomy and postsale equity ownership. Each confers advantages and disadvantages concerning your equity stock’s upside, liquidity, and interface with your practice’s performance.

The distribution waterfall is another domain that varies. Figure 3 summarizes an example waterfall.2 For context, debt obligations are often senior to equity obligations. If the debt component of enterprise value increases with higher interest rates, then the equity stock component is commensurately decreased.

Consultants can systematically model these financial complexities with forecasts that estimate the long-run value generated or lost by partnering with a DSO or DPO. Forecasts synthesize the specific terms of the deal, including management fees and tax implications, under various scenarios for practice and equity performance. We use a sensitivity analysis to posit how different equity growth projections impact your long-run financial position. As advisors, our role is to be data-driven and inculcate you with knowledge to ensure an organization’s terms and culture align with your goals.

Negotiations

Most transactions involve some level of negotiations. While no formula is applicable to every situation, we recommend channeling negotiations through advisors. With that responsibility, it’s imperative for advisors to understand the underlying interests for each party and, preferably, discuss multiple negotiation issues simultaneously. By taking a comprehensive approach at the onset, consultants can unpack which issues are interrelated and which are most important to each side.

Once identified, the various features of a deal can be prioritized to form a decision matrix. Examining each issue separately can foment unnecessary competition, as the current topic being discussed can artificially become the most critical, since it’s the only detail commanding attention at that time. Holistic conversations identify integrative issues, empowering cooperation to expand the pie for mutual gain. For example, if a seller’s top priority is sales price and a buyer’s top priority is timetable (e.g., graduation date), then the buyer may offer concessions on sales price if the seller is willing to accelerate the transition date.

As advisors, we advocate for a precontract meeting between the seller and the buyer after the letter of intent (LOI) is signed and financing is secured. The precontract meeting provides an opportunity for all parties to find agreement on the granular details not fully encompassed in the LOI. Not only does this step streamline the rest of the process, but it also curbs attorney fees by addressing particulars of the deal before attorneys are involved.

Preparation and planning

Planning in advance for a practice sale will often reward the seller with a higher valuation and a more seamless process. This begins with a quality of earnings (QoE) process to elucidate the level and sustainability of operating CFs. QoE integrates data from tax returns, financial statements, and practice reports. Since appraisals derive from business profits, QoE informs strategies to refine administrative or clinical activity now to boost valuation later. To increase revenue, sellers can improve billing/collections workflows to reduce A/R, offer new services, change service mix, negotiate reimbursement rates with insurance, and refresh marketing campaigns. To increase efficiency, sellers can examine fee structures with suppliers, modify schedules, and enhance new-patient intake processes and case presentations. Some of these will optimize profitability with the same amount of clinical work. Furthermore, we can help identify the ROI of potential projects to modernize the office and bolster the future sales price. We can also guide succession planning, including whether to hire an associate doctor as a prelude to sale. Sufficient preparation will help adhere to the desired exit timetable.

Editor's note: This article appeared in the March 2026 print edition of Dental Economics magazine. Dentists in North America are eligible for a complimentary print subscription. Sign up here.

References

- Esmer B. Leveraged buyout modeling fundamentals. The finance of buyouts and acquisitions. The Wharton School of Business. Spring 2024.

- Lehman R. Distribution waterfall. Moonfare. Updated November 28, 2025. https://www.moonfare.com/glossary/distribution-waterfall

About the Author

Keith Nicholson, DDS, MBA, MS

Keith Nicholson, DDS, MBA, MS, is an orthodontist who has been active in various domains of dentistry. He has owned a multilocation private practice, served as part-time faculty, and earned an MBA in finance from Wharton. He partners with peers to unlock their potential, aiming to streamline operations and optimize profitability while delivering excellent care. Additionally, Dr. Nicholson is a consultant with PMA Practice Transitions, appraising and selling dental and dental specialty practices.