How to get out alive!

Based on anecdotal evidence and my own observations, it looks like the average dentist can’t retire until about 4.3 years after he dies! Probably not what you had in mind. How do so many of us find ourselves in such a fix? Logically, we know a day of reckoning is coming. But knowing is not enough.

By one measure, 58 percent of the American population is overweight. Surprisingly, in spite of their knowledge, 56 percent of health-care professionals are overweight. We know we need to eat better and exercise more, but we are often missing the component of proactive commitment. (Sounds like a conversation about flossing, doesn’t it?)

What do you do once you are serious about making the commitment to be financially prepared for retirement? Here are some general steps, followed by more detailed discussion:

Saver or spender?

First of all, be honest with yourself. Are you a natural saver or a spender? Natural savers read an article like this one just for a few gems and to confirm many things they already know or do. So, savers, quietly talk among yourselves while I work with the other end of the spectrum. You spenders know who you are. This may be one of the times during the year when you goad yourself into perusing three to four issues of Dental Economics at one sitting. You don’t really want to, but you somehow know that you are supposed to. Saving money just isn’t your thing!

Secondly, recognize that you (and the saver) are possibly genetically wired to be the way you are. So, it won’t be easy changing gears. You will definitely have to move outside your comfort zone. Of course, if you are married, you and your spouse may have different styles to contend with, too. If you are not good at finances and the business aspects of your practice, the buck still stops with you. You may not enjoy those areas, but you should surround yourself with good advisors ... and insist that they show you enough to help you at least suspect what is going on!

Third, get a “fiscal” fitness coach - someone to encourage and nudge you ... and hold you accountable! (One of the big reasons Weight Watchers works is the fact that you know you will be weighed every Monday!) Ideally, a fee-only financial planner would be a good candidate. Fee-only financial planners don’t sell any products, so some folks argue that they provide unbiased advice. This may not be the same person who handles your investments, but it often is.

Fourth, develop a reasonable game plan. (As with losing weight, you need a lifestyle change, not the latest fad diet.) If you are faced with eating an elephant, take it slow, but steady ... and do it one bite at a time. As Yogi supposedly said, “If you don’t know where you are going, then you might not get there!” (Sometimes I think it would take three lifetimes for Yogi to have said all the things attributed to him.)

Now, let’s look at some particulars:

How much do you need to live on?

I am working with a client who makes $400,000 annually in take-home pay. The client and his wife diligently pored over their personal checkbook to arrive at their annual spending. They came up with $350,000. They had blank looks on their faces when I asked them where the “extra” $50,000 was that they should have saved. It obviously was nowhere to be found, so they went back to the books one more time.

Whether you track your income and expenses manually or via computer, you should do a “proof of cash” for the year (or other time period) to check your results. Start with the balance in your checking account(s) as of, say, January 1. Add all revenues received and subtract all expenditures. Theoretically, you should end up with a figure that matches the bank balance at the end of your test period, say, June 30. If the revenues are greater than your “income,” then you need to identify deposits that may have been transfers from other bank accounts, brokerage accounts, sale of stocks, etc. Also, identify any disbursements which were not true expenses, but which may have been transfers to other accounts. (I’ll let you know if/when we find the extra $50,000.)

Once you know your income/expense requirements, you can determine how much your practice needs to gross to net the required income. Your dental CPA can help you with this.

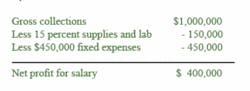

For example, suppose your recurring (“fixed”) expenses are $450,000 per year. This includes everything except “variable” production expenses (supplies and lab fees) and never includes the doctor’s own wages. The fixed expenses include things such as staff wages, facility, and administrative expenses. Further, assume that your variable production expenses (supplies and lab) total 15 percent of your collections. (Since they vary as your production level changes, they are stated as a percentage vs. a dollar figure.) Technically, this should be stated as a percentage of the production, so this may not appear directly on your practice’s profit and loss statement.

The production/collections required to cover all expenses, plus your desired “salary,” is the break-even point. This figure equals (Salary and Benefits + Fixed Expenses)/(1-variable expense percentage). Using the figures above, break even = ($400,000 + $450,000)/(1 - .15) = $1,000,000. The proof is as follows:

null

Your dental CPA would apply some of that net profit to tax-deductible fringe benefits and a retirement plan, before declaring an amount for your taxable salary. For example, if you need to net $50,000 more, then you need to increase your collections by $50,000/(1 - .15) = $58,824. Although your fixed overhead has already been paid, you still need to gross enough to pay for the supplies and lab on the extra production in order to “net” you an extra $50,000. So the amount of your current expenses plus additional savings determines your break-even point. The amount you need to be saving is covered next.

How much do you need to retire (or accumulate for other major expenditures)? This is not a fixed amount and needs to be revisited once a year or so. Things like rate of inflation, investment returns, and time horizon come into play. A very rough rule of thumb says that to retire today, you need about $250,000 of investment funds on hand for each $1,000 per month you require. This amount assumes you want the funds to last 30 years and to provide you with a 3 percent raise every year in retirement. To retire 10 years from now, you need about $333,333 for each $1,000. To retire in 20 years, you need about $500,000! The required amount increases in the future due to inflation. But, the good news is that you have more years to accumulate those funds.

Here are a few thoughts to keep in mind. The above amounts do not include the value of your house, since you have to live somewhere. The amounts do include the after-tax value of your practice, since you will sell that. To be more precise, you need to look at the nature of your investments. For example, how much do you have in retirement plans vs. funds held personally? The retirement funds will be taxed as you spend them, whereas personal investments only pay tax on any future gains.

There is continual discussion among financial advisors about how much you can safely withdraw from your investments each year and not deplete the funds. It is not as simple as saying that if you earn an average 7 percent return on your investments, then you can withdraw 7 percent per year. That assumes that you earn 7 percent every year. Noted Nobel laureate in economics, Paul Samuelson, says that you can’t wade across a river just because the average depth is four feet!

Let’s say a doctor retired in 1967 - just before the market went into a prolonged bear market. He withdrew 7 percent every year, but he ran out of money in 14 years! He did not take into account the yearly variation in investment returns ... and he happened to retire at the wrong time! A more sophisticated analysis would involve using “Monte Carlo” techniques (see my May 2002 DE® for more about these techniques).

This was developed while doing research for creating the nuclear bomb in the Manhattan Project. The scientists did not have a formula to determine the path of a specific nuclear particle. However, if they watched enough particles in a cloud chamber, they could see a pattern that would allow them to predict the path with a certain degree of accuracy.

In a similar manner, computers can run several thousand scenarios of possible investment outcomes for the future. (They can see a pattern based on up years and down years. From that, they can tell if your particular financial plan has a 95 percent chance of success, like the solid line in the graph.) If you insist on withdrawing more money, then the chance of success might drop to, say, 70 percent.You can then set your withdrawals based on your risk tolerance level.

In December’s column, we will discuss how you can accumulate the required funds - “Man at Work and Money at Work” - using the term “man” loosely. Meanwhile, start working on what your current income requirements are.Raymond “Rick” Willeford, MBA, CPA, CFP®, is president of Willeford Haile & Associates, CPA, PC, and Willeford CPA Wealth Advisors, LLC. As a fee-only advisor, he has specialized in providing financial, tax, and transition strategies for dentists since 1975. Mr. Willeford is the president of the Academy of Dental CPAs, a consultant member of AADPA, and is available as a speaker nationwide. Contact him by phone at (770) 552-8500 or by e-mail at [email protected].