Customize payment options to increase patient satisfaction and retention

You always focus on providing the best care for your patients, and you know this commitment extends beyond the scope of the procedure. A friendly chairside manner, cheerful customer service before and after treatment, sedation options, and even streamlined online booking all help create a positive patient experience.

When practices focus on the entire experience, everyone benefits. Not only does the patient feel genuinely cared for, but a happy patient who enjoyed their time with you is both more likely to return and spread the good news of your practice via reviews or word of mouth, expanding your business.

One component that can vastly improve patient satisfaction is how payment options are handled and discussed, specifically when it comes to financing. While some practices may find broaching these discussions uncomfortable, others have found that patients appreciate an upfront and frank discussion on payment options, leading to a better overall experience.

Practices that took it a step further found that customizing the conversation based on the treatment plan’s cost resulted in even greater patient satisfaction as patients were presented with the best available option for their unique situation.

What type of patient financing solution should you be offering?

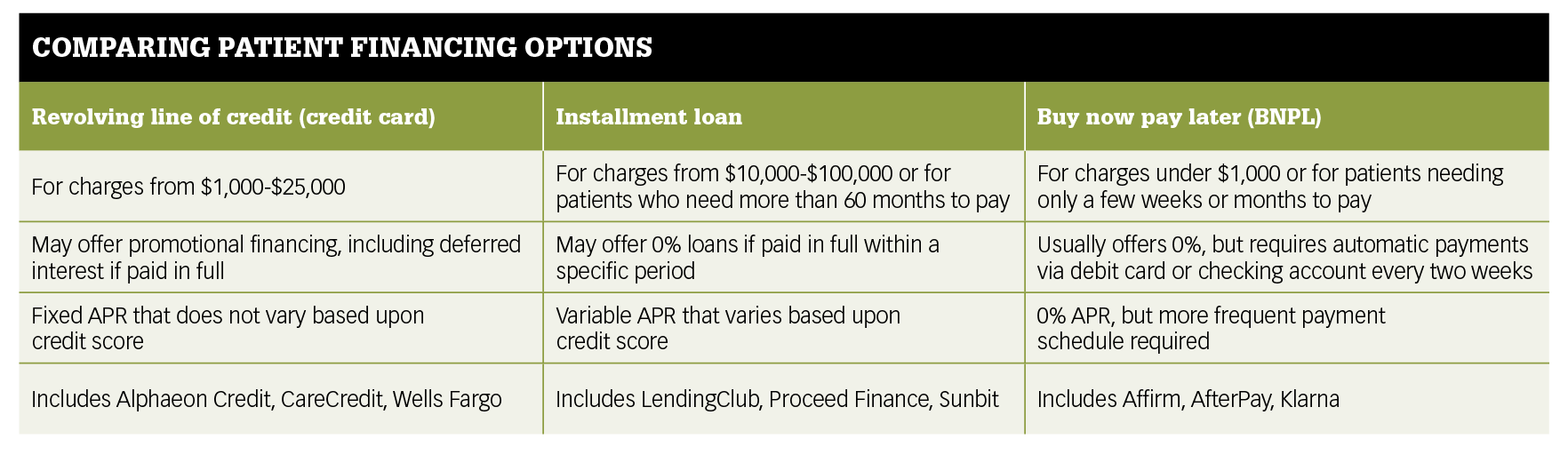

There are types of patient financing options:

- Revolving lines of credit

- Installment loans

- Buy-now-pay-later products

Revolving line of credit

The most commonly used patient financing option in dentistry today is a revolving line of credit in the form of a credit card for health-care purchases, such as Alphaeon Credit, CareCredit, and Wells Fargo. Unlike other credit cards, private-label credit cards like these can only be used within a network of practices that have agreed to accept that card. With a revolving line of credit, when a patient applies and is approved, they are provided with a credit card with a specific credit limit. The patient can reuse this line of credit repeatedly to pay for any treatments or services that are within their credit limit.

Related content:

3 steps to implementing interest-free patient financing

5 effective ways to increase case acceptance

An additional advantage is that all of these companies offer promotional financing options with deferred interest if paid in full within 6, 12, 18, or 24 months or equal payment plans with a lower fixed APR for up to 60 months. Some companies, such as CareCredit, may vary the APR based on the selected promotional plan. Private-label credit card companies can offer credit limits as high as $35,000.

Tony Seymour, president of Alphaeon Credit, says, “While we issue credit limits as high as $35,000 in dentistry, I like to say we are the workhorse for the practice. We aren’t necessarily who you use for a full-mouth restoration, but we are who you use daily for all other types of cases and treatments. Today, we finance an average of $3,500, but our credit limits are usually double that amount.”

Even if the patient does not receive a sufficient credit limit to cover their treatment plan’s total cost, many dentists continue to offer revolving lines of credit because the patient can set up their treatment plan and pay in stages. As the patient pays down the balance, additional funds become available for future treatment expenses.

Practices also appreciate the ability for the card to be shared among family members and loved ones, increasing the number of patients they can treat. Periodic credit limit increases can also be available to patients with strong payment history. Another wonderful benefit of revolving lines of credit is that your patient knows they always have financing available that is compatible with your office, thus increasing the possibility of provider loyalty and making them less likely to shop around for treatments.

Installment loans

Unlike revolving credit that can be reused, installment loans are considered a “one-and-done” type of loan. Some of the installment loan lenders today in the dental space include LendingClub, Proceed Finance, and Sunbit. With installment loans, the patient applies for a specific amount and agrees to pay the loan back within a specified period. The funds initially lent cannot be reused after repayment. If the patient wanted to use the same lender, they would have to reapply.

One benefit of installment loans is that the interest rates can be low. However, the interest rate with installment loans vary by patient, based on credit score, from an average of 8.9%, but some lenders charge as high as 36% (or, in the case of subprime lenders, even higher).

While revolving lines of credit theoretically never expire, promotional plans do—most companies only offer up to a 60-month term. Installment loan lenders often have the ability to go beyond 60 months, making them best suited for extremely high-ticket charges such as full-mouth restorations costing over $35,000. (See chart below.)

{kind=link}

Buy now pay later

The latest entrant to the patient financing space for dentistry is buy-now-pay-later (BNPL) providers. First popularized by online retailers and companies such as Affirm and Klarna, BNPL is used for smaller purchases that can be repaid very quickly. Unlike revolving lines of credit and installment loans that are repaid monthly, BNPL products are often paid biweekly or even weekly in some cases. As the payment schedule is more aggressive, this type of product is best used for treatment plans under $1,000 or for patients who can quickly pay off the total cost of their care in just a few months.

Keep in mind, the BNPL industry is new and is not as regulated as credit cards or installment loans. If you are offering membership plans (which credit card and installment loan companies might discourage as it is considered prepaying for services that won’t be provided within 30 days), this might be a good option for those types of charges.

If your treatment offerings vary in price range, consider customizing the payment options presented to the patient based upon cost, versus a one-size-fits-all mentality. Pairing the treatment plan with a particular financing plan based on cost may make all the difference to a patient’s ultimate satisfaction, helping both the patient and your practice.

Editor's note: This article appeared in the September 2022 print edition of Dental Economics magazine. Dentists in North America are eligible for a complimentary print subscription. Sign up here.

About the Author

Katy Thomas

Katy Thomas has over 20 years of experience in the patient financing space. She is currently vice president of marketing for Alphaeon Credit.