Profit down, overhead up (a lot): Findings from the 2022 Dental Economics/Levin Group Annual Practice Survey

For the 17th consecutive year, the team at Levin Group is pleased to work with the editors at Dental Economics to provide our profession with important insights on the state of dental practice. Many thanks to those dentists who provided valuable information about their practice’s successes and challenges in 2022.

This year’s data was collected from general dentists in early January 2023. Ninety percent of the respondents were practice owners and/or partners. We asked respondents to consider their full-year 2022 practice performance when answering the survey questions.

2022 brought many new challenges to dentistry, the combination of which we have never seen before. Inflation, staff shortages, increased labor costs, declines in average practice profitability, and other factors were notable, especially when compared to 2021. Before diving in, here are a few historical facts and realities from previous Dental Economics–Levin Group Annual Practice Surveys:

- In 2008–2009, the US experienced the deepest and longest recession in history. Production in the average general dental practice declined by approximately 10% during that time, but there was no commensurate increase in overhead to impact profitability, nor were there other factors that had negative effects on dental practices.

- In 2012, the US economy began an excellent run that lasted through 2021, even during the pandemic. Dental practices overall thrived, and each year represented an increase in average practice production and profitability, even though dental insurance reimbursements were often stagnant or in some cases declined. The propulsion of an excellent economy allowed dental practices to expand. Other strategic factors such as adding new services or technologies also helped to increase practice production during this time. Overhead increased, but at consistent, acceptable rates and did not have a negative impact on practice profitability.

- 2021 was an outlier and an amazing year. Most dental practices grew in production and profit—a high percentage had record production and profit. This was not due to any specific changes in practice operations or innovations in dentistry. It was mostly due to the American public having excess financial capability due to more savings accumulated during the pandemic, when consumers were not spending money in four traditional areas (travel, entertainment, restaurants, and luxury). Some of this excess was spent in dental practices, many of which had significant backlogs in scheduling patients. All of this led to an excellent (and in many cases, record) year in 2021.

- Then 2022 arrived. The year came with a challenging economy, inflation, higher interest rates, rising staffing costs, staff shortages, and higher no-show rates as patients recognized that the excess cash they had enjoyed a year before was now dissipating. It also brought with it a production drop of almost 10% in many practices. Unlike the 2008–2009 recession, the production drop in 2022 was accompanied by an average increase of 5%–6% in practice overhead. This is a key point to keep in mind as you read through this year’s survey results.

You might also be interested in ... Surviving (even thriving!) in 2021

Overhead increased (a lot)

Rising overhead is the major theme in this year’s results. Remember that every 1% increase in overhead equates to a 1% decrease in practice profitability. Therefore a 5% increase in overhead means the loss of $5,000 of profit or income for every $100,000 of production. That would be a $50,000 loss of profit or income in a practice with a production of $1 million.

What does that mean?

The survey indicated that in 2022, 70% of practices reported higher production in 2022 versus 2021. On the surface that sounds encouraging; however, last year in our survey of 2021 performance, more than 90% of practices reported higher income over the previous year. 2021 was a banner year for production in most dental practices. There was pent-up demand from the pandemic, and patients had significant disposable income to spend on their dental needs. It is not surprising that this year fewer practices reported increased production. What is surprising is the decline in the number of dentists who reported large increases in production in 2022:

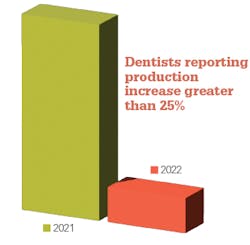

- Only 4.6% of dentists reported that their production increase in 2022 was greater than 25%. This is a significant decline from the 25.7% of dentists who reported a 25% or more increase last year.

- Only 31% of dentists reported that their production increase in 2022 was greater than 10%, which is about half of the 64.9% that reported that level of increase in the previous year.

So, not only did fewer practices report increased production this year, but the size of the increase was significantly lower. Even taking into consideration that 2021 was an unprecedented growth year for many practices, it still appears that 2022 was a much more difficult year for dentistry regarding production increases.

You might also be interested in ... Trends and challenges that will reshape the dental profession

Production is important, but profitability is what feeds the bottom line. It’s what practice owners get to keep or use to grow the business. And profitability appears to be declining. Seventy percent of practices reported an increase in production, but only 56.1% reported an increase in profit. This was directly due to increases in overhead and higher expenses.

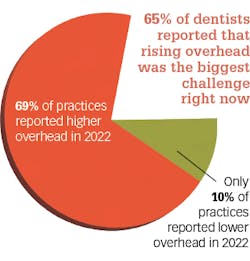

In 2022, 69% of practices reported higher overhead. Only 10% of practices reported lower overhead. When asked “how much higher” overhead had increased, one-third of respondents reported that it had grown by 10% or more. Of the 69% who said their overhead was higher, the average increase was 8.6%. The average overhead increase of all respondents (including those who reported the same or lower overhead) was 5.9%.

Not surprisingly, 65% of dentists reported that rising overhead was the biggest challenge right now. This was the number one response from a list of eight top challenges that respondents could select, and it was by far the predominant factor.

Levin Group insight

2022 appears to be the first year in dental history with profitability challenges combined with increasing overhead. And this is the major takeaway from this year’s Dental Economics–Levin Group Annual Practice Survey. Staffing challenges, inflation, supply chain issues, and higher pricing by suppliers and vendors are all contributing to higher overhead. Fortunately, dentistry has been able to continue to provide services for patients and attract new patients at a level that kept production stable or growing in 2022. The challenge for the future is how to compensate for overhead increases.

Indications are that 2023 could be a slower production year as the economy stays challenged, interest rates continue to rise, and consumers spend down their savings. Practices need to focus on identifying strategies to increase production and offset rising overhead, which will allow them to maintain or increase practice profitability.

The government stimulus programs are now gone, and patients are back to spending money in the traditional areas of luxury, entertainment, restaurants, and travel. Consumers are using up their excess savings as evidenced by rising credit card debt, and they’re spending more money in market segments other than dentistry. This explains why production has grown at a slower rate and profitability has generally declined across-the-board.

Where dentistry was “treading water” from a profit standpoint in 2020 and had significant increases in profitability in 2021, it is now experiencing a downturn in profitability. If production is stable or slightly lower in 2023 and overhead keeps increasing, then maintaining 2022 profit levels will also be a challenge. Updating practice systems is one of the best approaches to improve overall efficiency, train the team at the highest level, maintain high production, and help control and reduce overhead. We encourage practices to focus on this now.

And now for the team

It will not surprise anyone that practice staffing is more challenging than ever. There had been a slight shortage of staff prior to the pandemic, but now the entire situation has reached crisis level. One obvious example of this is the shortage of dental hygienists. Levin Group estimates that 10% of dental hygienists have left the profession, and most of those will not return.

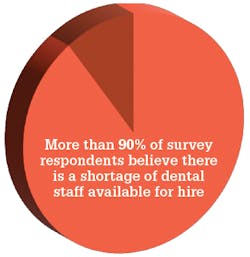

More than 90% of survey respondents believe there is a shortage of dental staff available for hire. Sixty-five percent stated that they are currently seeking to hire one or more staff members. This number is the same as in 2021, reflecting a chronic condition with no evidence of improvement. Forty-nine percent of practices state that they currently have one open position, and 22.7% of practices lost more than one team member in 2022.

No dentist or office manager will be surprised that staffing is viewed by most practices as “very challenging.” On top of the shortage of qualified applicants, the cost of staffing has risen almost 10%, which is a major contributory factor to the reported higher practice overhead.

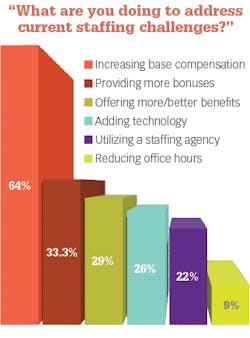

Levin Group asked practices, “What are you doing to address current staffing challenges?” Respondents identified the following strategies:

- Increasing base compensation for staff (64%)

- Providing more bonuses for staff (33.3%)

- Offering more and/or better employee benefits (29%)

- Adding technology for productivity enhancement (26%)

- Utilizing a staffing agency (22%)

- Reducing office hours (9%)

Note that the top three strategies are all relative to increasing total staff compensation, which directly increases practice overhead.

Levin Group insight

Staffing has continued as a crisis in dentistry. Many team members resigned during the pandemic. Most of those who left the profession have not returned, contributing heavily to the staffing shortage. Those who took new positions had numerous reasons, but the most impactful was higher compensation. As practices have started playing catch-up in providing competitive compensation, they have been able to attract new team members, but the rate of those resigning positions and changing jobs is still high.

The increase in staffing compensation will not reverse, and its impact on overhead will remain. From a business standpoint, practices should focus on designing specific strategies to offset increases in staffing compensation. Examples include raising fees, submitting new fee schedules to insurance companies to increase profiles, cross-training team members for coverage if a team member were to leave, implementing highly efficient step-by-step systems to eliminate waste and maximize efficiency, and adding advanced team training. A team functioning at the highest level of efficiency can offset rising overhead costs.

No one knows exactly how the staffing crisis will play out. Levin Group estimates that it will be a major challenge in dentistry affecting practice production and profitability for many years to come. Practices should implement innovative ways to retain team members. Signing bonuses, longevity bonuses, more paid time off, and job sharing are all becoming part of the norm.

Impact of insurance company behavior on production, profitability

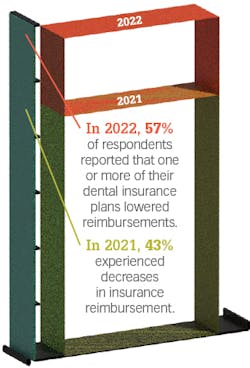

Fifty-seven percent of respondents reported that one or more of their dental insurance plans lowered reimbursements in 2022. This is a 14% increase over the number who experienced decreases in insurance reimbursement in 2021, so that trend appears to be continuing.

These lower reimbursement levels have a direct impact on profitability. About half of those who reported a decrease this year told us it was greater than 5%. Given that nine out of 10 respondents reported participating in insurance, a 5% decrease in reimbursements will have a negative impact on production.

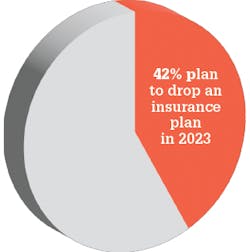

When asked if practices plan to drop any insurance plans in 2023, 42% responded affirmatively. While this seems extremely high, it indicates the frustration that dentists have with insurance companies, many of which are lowering reimbursements at a time of higher inflation, higher staffing costs, staff shortages, and other challenges.

Levin Group insight

Dental insurance companies have a different orientation than dental practices; it is often an antagonistic relationship. Ideally, insurers would raise reimbursements as overhead in dental practices rises. This is not the case, and many of the dental insurance maximums have barely risen in the last 30 years. We expect dental insurance companies to continue to lower reimbursements, restrict maximums, and follow a very strong cost-containment mentality. This is not a moral or ethical decision by dental insurers; it’s a business and financial one. Dental insurers do not consider factors such as practice success and doctor income when establishing their reimbursement schedules.

It is not surprising that many insurance plans have reduced reimbursements. This is a standard operating approach by some insurers and has been an ongoing trend for many years. Practices need to evaluate and analyze their insurance participation each year to determine the right mix of fee-for-service dentistry versus insurance plan participation. If reimbursements continue to decline, practices will need to increase patient volume, maximize practice efficiency through excellent business systems, and add new noninsurance-covered services.

A few other interesting findings

- Forty-seven percent of practices reporting having patients enrolled in an in-house dental membership plan. That is slightly higher than in 2021.

- Eighteen percent of practices reported seeing an increase in the amount of third-party patient financing being used to pay for dental treatment.

- Fifteen percent of practices reported they currently use some form of teledentistry to serve patients remotely. This was the same as in 2021.

Levin Group insight

We were not surprised that third-party patient financing has been growing, and we believe it will continue to in 2023. Credit card debt is once again rising as Americans have gone from significant savings during the pandemic to having spent that savings and needing to access credit for larger expenses. Dental practices should ensure that every patient is aware of any third-party financing available in the practice. Third-party financing is additional access to debt for patients and will play an increasingly major role in dentistry.

In-house dental membership plans are also growing and have established their place in dentistry. They create a sense of value for patients and a monthly revenue stream for the practice. However, one of the best benefits of an in-house dental membership plan is patient retention. Patients have a feeling that they belong at the practice. Although participation in dental membership plans is currently growing slowly, we believe there will be a tipping point where participation begins to accelerate even faster.

Teledentistry use in general practices has remained stagnant. There is less opportunity for general dentists to effectively use teledentistry than other areas of dentistry, such as orthodontics. This is why we were not surprised to see that the use of teledentistry has not grown, and we don’t expect it to grow much in the near future.

Summary

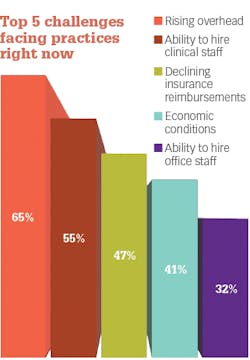

We asked survey respondents to identify the biggest challenges facing their practice right now. The group responded with their top five:

- Rising overhead (65%)

- Ability to hire clinical staff (55%)

- Declining insurance reimbursements (47%)

- Economic conditions (41%)

- Ability to hire office staff (32%)

This year’s Dental Economics–Levin Group Annual Practice Survey was certainly unique. What we saw was slightly rising production with decreasing profitability due to increasing overhead. This is the first time we’ve seen this scenario in dentistry and unlike any previous era of uncertainty, including the Great Recession of 2008–2009.

One of the strongest contributory factors behind rising overhead is staffing costs. Not only have staffing costs risen, but managing the entire staffing process (recruiting, hiring, retaining) has become an emotional and fatiguing daily frustration. Not having the right number of trained staff simply makes day-to-day dental practice harder.

But staffing is not the only area of overhead increase. Inflation has driven up the cost of supplies, materials, and technologies as well. The 10% rise in staffing costs combined with other increases and inflation contributed to a 5%–6% overall increase in practice overhead in 2022. This results in a direct reduction in practice profitability. Practices need to identify systems, strategies, and methods to ensure increasing production to offset rising overhead.

Dentistry is still in an extraordinarily strong financial position from a business standpoint. Production did grow in 2022, and collections remain stable.

Many practices still have a schedule backlog. One practice we know recently held a “hygiene-only day,” bringing in temporary hygienists and utilizing all three doctors to do hygiene. They ran nine operatories of hygiene for an entire day to help catch up on patients and keep any from feeling they could not get appointments and risk them leaving for other practices. Examples of this type of innovative thinking are helping practices improve performance, maintain patients, attract new patients, and maintain excellent financial performance.

2023 is starting out with a continuation of the challenges we saw in 2022, but we are optimistic that by 2024 the economy will stabilize, allowing dental practices to return to higher growth in practice production to offset higher expenses and inflation.

We look forward to seeing how that prediction plays out in next year’s Dental Economics–Levin Group Annual Practice Survey. Be sure to join in again!

Editor's note: This article appeared in the April 2023 print edition of Dental Economics magazine. Dentists in North America are eligible for a complimentary print subscription. Sign up here.

About the Author

Roger P. Levin, DDS, CEO and Founder of Levin Group

Roger has worked with more than 30,000 practices to increase production. A recognized expert on dental practice management and marketing, he has written 67 books and more than 4,000 articles, and regularly presents seminars in the US and around the world. To contact Dr. Levin or to join the 40,000 dental professionals who receive his Practice Production Tip of the Day, visit levingroup.com or email [email protected].