Which entity is right for your practice?

Dental professionals frequently ask about the best entity choice for dental practices. While there are a number of relevant considerations in choosing an entity, or multiple entities depending on your circumstances, the decision is most often driven by tax considerations. The tax consequences will differ depending on whether the practice is operating as a C corporation, S corporation, or in an unincorporated form, such as a sole proprietorship, general partnership, or LLC that has elected not to be taxed as an S corporation.

C corporations have historically been popular with doctors. A C corporation is a separate taxable entity, and any profits remaining in the corporation at year-end are taxed at a flat federal income tax rate of 35%. They are taxed again if and when those profits are distributed to shareholders as dividends. Due to concerns with this "double taxation" on practice profits and sales proceeds, along with recent guidance that discourages "zeroing out" the corporation with bonuses, very few doctors continue to operate as a C corporation.

RELATED ARTICLE:Did you know your dental practice LLC can be taxed 4 different ways?

The most popular entity for dental professionals is the S corporation, due to the ability to control payroll taxes. S corporations must pay reasonable compensation to the doctor/shareholder for services provided, which is subject to payroll taxes. Doctors can generally avoid an IRS attack by paying themselves a salary equal to the greater of the maximum compensation considered for retirement plan purposes ($265,000 for 2016), or 25% of collections. Any remaining corporate profit can be paid out as a dividend, free of federal and state payroll taxes. This allows the doctor to avoid some of the 2.9% Medicare portion of the payroll tax and the Obamacare-imposed 0.9% Medicare surtax on wages in excess of $250,000 for married doctors.

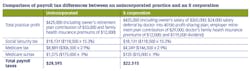

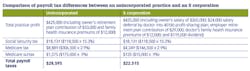

In contrast, for doctors operating in unincorporated form, all practice profits are subject to self-employment (SE) taxes. Moreover, health insurance premiums for the doctor's family and retirement plan contributions made on the doctor's behalf are included when computing the profits subject to SE taxes. Those items are not subject to payroll taxes in an S corporation except salary deferrals by the doctor/shareholder into his or her 401(k) profit sharing plan. Table 1 is a comparison of the payroll tax differences between an unincorporated practice and a practice operating as an S corporation.

Note that, although the annual practice profit is the same for both practices, in the S corporation the practice-paid retirement plan contribution, health insurance premiums, and dividends escape payroll taxes, resulting in $6,080 in annual payroll tax savings compared to an unincorporated form.

Doctors currently utilizing a C corporation or unincorporated form should discuss with their professional advisors whether, after considering other relevant factors, a switch to an S corporation is right for them. It is neither complicated nor expensive for an existing LLC to elect to be taxed as an S corporation. C corporations can also elect to be taxed as S corporations. While such election is slightly more complicated, through proper planning it can be done with little cost and hassle. It is also essential to consult with your tax advisor on state income and franchise tax concerns that may alter the conventional wisdom that applies in most jurisdictions.

Patrick Craig, JD, provides legal services through McGill and Hassan PA. John K. McGill, JD, CPA, MBA, provides tax and business planning exclusively for the dental profession and publishes the McGill Advisory newsletter through John K. McGill & Company Inc. Both are members of the McGill & Hill Group LLC, your one-stop resource for tax and business planning, practice transition, legal, retirement plan administration, CPA, and investment advisory services. Visit mcgillhillgroup.com.