How to select the correctretirement plan for your practice

For more on this topic, go to www.dentaleconomics.com and search using the following key words: retirement planning, 401(k), SIMPLE-IRA, profitability, John K. McGill.

One of the most common retirement plan mistakes dentists make is sticking with the same retirement plan, despite changes in the doctor’s age and profit levels. Unfortunately, it’s not uncommon to find a dentist with a retirement plan that not only does not meet his or her retirement objectives, but has not for the last five, 10, and sometimes 20 years, says Jason Arnold, East Coast manager of PenSys, Inc., a retirement plan consulting firm that specializes in assisting dentists nationwide.

As doctor’s age and practice income increases, the plan design should be evaluated at least every five years to maximize owner benefits, says Arnold. Plan changes may involve plan type, provisions, or the addition of a second plan.

The most common progression of retirement plan designs for doctors is: 1) SIMPLE-IRA, 2) Integrated Profit Sharing Safe Harbor 401(k), 3) Class Allocation Safe Harbor 401(k), 4) Defined Benefit or Defined Benefit / Safe Harbor 401(k).

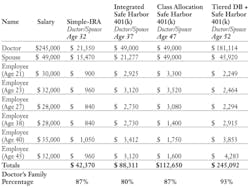

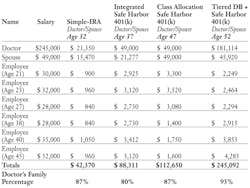

SIMPLE-IRAs work best for doctors with limited funds to save (less than $30,000 annually). In this design, employees can defer up to $11,500 of their income into the plan (plus an additional $2,500 if age 50 or older), with contributions matched by the practice dollar for dollar up to 3% of pay. This plan can be effective, but for a dentist earning the maximum allowable salary of $245,000, the maximum possible contribution is limited to $21,350.

As practice profitability increases, the transition to a 401(k) plan will allow increased funding through profit sharing contributions. The maximum contribution to a 401(k) is $49,000, including a combination of employee salary deferrals and employer contributions. Salary deferrals are limited to $16,500 (plus an additional $5,500 if age 50 or older). If there is limited disparity in age between dentist and staff (less than five years), a profit sharing formula integrated with the Social Security Wage Base will provide larger contributions of $49,000 for doctor and $21,277 for spouse, or 80% of the total (see chart).

As practice profitability and disparity in age between dentist and staff increases, a change from the Integrated to Class Allocation profit sharing formula is optimal. This can increase contributions for doctor and spouse to $98,000, or 87% of the total (see chart).

The final plan design progression for most doctors is usually to a Defined Benefit or Defined Benefit/401(k) combination. This works well for practices with a history of excellent profits, and allows for the largest contributions over the shortest period of time. The required contribution under these plans is actuarially calculated each year and not subject to the annual contribution limits applicable to SIMPLE or 401(k) plans. The total owner contribution for a DB/401(k) combination plan can be as much as $227,034, or 93% of the total.

Every dentist may not follow the most common progression of plan designs discussed here; however, Arnold says dentists CAN avoid getting stuck in plans that no longer meet their retirement goals by having the plans reviewed at least once every five years.

John McGill provides tax and business planning exclusively for the dental profession and publishes “The McGill Advisory” newsletter through John K. McGill & Company, Inc., a member of the McGill & Hill Group, LLC. Arnold provides retirement plan design and administration services through PenSys, Inc., at (888) 440-6401, an affiliate of the McGill & Hill Group — a one-stop resource for tax and business planning, practice transition, legal, retirement plan administration, CPA, and investment advisory services. For more information, visit www.mcgillhillgroup.com.